Supply Analysis Update

An update on ICP Supply dynamics

Background

In early January I published a review of the ICP supply dynamics. I also combined the supply analysis with demand drivers to get a full picture of the ICP supply-demand dynamics over the next few years. Now that almost three months has past since my original supply analysis, let’s review whether the analysis still holds true, what’s coming up in the near future and any dynamics that may affect ICP price.

Where we are at today

In the original article, I explained the three sources of ICP coming into the circulating supply:

Node Rewards paid to node operators

Governance rewards paid to ICP-stakers on the NNS

Dissolving ICP of neurons on the NNS

January and February saw 44k and 79k ICP in node rewards, respectively. This is inline with the 60k ICP/month in 2021. March’s total will almost certainly be greater than 60k, however node rewards are still not a major source of ICP supply into the circulating supply.

An average of 916k ICP per month has been minted as governance rewards in 2022 so far. We don’t know what percent of that remained on the NNS as merged maturity and what percent was sent to exchanges, but we do know that the minting increased slightly after the major governance changes went into effect in mid-February. I believe this is because the NNS participants who are actively participating in governance are also more likely to be doing something with their maturity (merging it or spawning it), whereas the participants who are letting their maturity accumulate are less likely to be voting or following a neuron on governance topics. For the sake of this article, let’s assume 50% of minted governance ICP is being sold on exchanges, so approximately 460k ICP/month is being added to the circulating supply. I, for the record, am a weekly maturity merger.

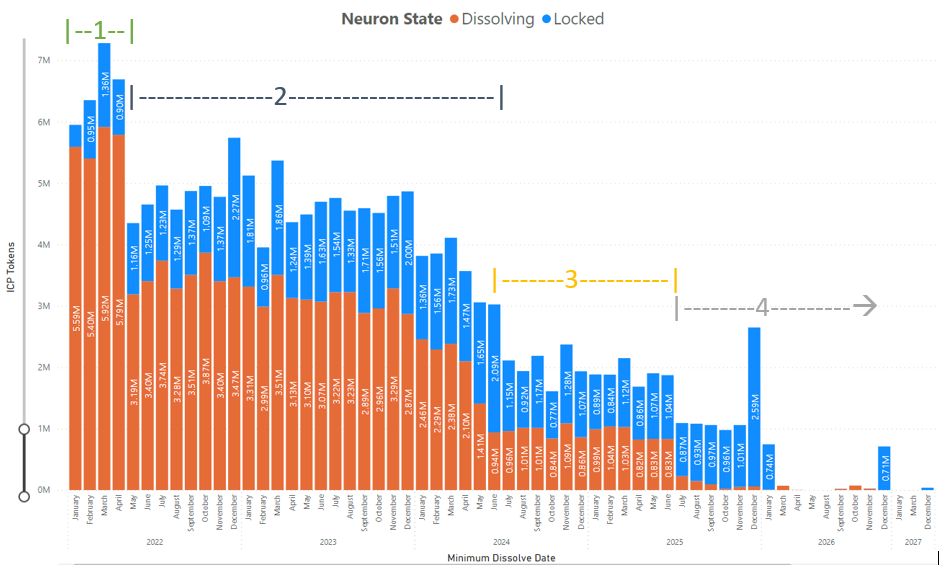

Finally, the main driver (~90%) of ICP hitting circulation (aka exchanges) is the amount of ICP dissolving off the NNS. The first three months of 2022 saw an average of 5.6M ICP dissolve off the NNS, in what I termed as “Zone 1” in the original article. This is primarily due to neurons 4008-4012, which contained over 3M ICP each. Luckily, we only have another month and a half until we are out of Zone 1 and into the much reduced supply of Zone 2. WAGMI.

What’s next

It typically takes ~4 weeks for a large dissolved neuron to disburse its ICP, so Zone 1 could last until late-May. However, from late-May onwards we should see a significant reduction in ICP dissolving off the NNS, to the tune of a ~2M ICP/month reduction. Zone 1 certainly had an affect on the ICP price, both in USD terms and relative to Bitcoin and Ethereum, as the price of ICP fell from around $40 to the high teens. I would expect that leaving Zone 1 would have a beneficial impact to price of ICP. How much impact? Well, prior to Zone 1, ICP was range bound between ~$40 and $60. There’s good arguments for ICP to trade above that range and there’s good arguments for ICP to trade below that range:

Arguments for ICP to Trade greater than $40-$60:

Real demand - There were minimal ICP demand drivers prior to entering Zone 1. However, as we leave Zone 1 we already see demand for ICP as a medium of exchange growing rapidly in NFT marketplaces. We also see the green shots of demand for DeFi with Sonic App burning 60k+ ICP in the past 2 months. In total, we have approximately 50k ICP more demand per month leaving Zone 1 than we had entering Zone 1. And that number is increasing rapidly.

Technological Progress - Technological risks have decreased in the past five months as Dfinity has delivered on key initiatives in the Titanium update, including ICP held in canisters and a developer’s preview of bitcoin integration, with production-scale deployment scheduled in early Q2. In addition, the NNS-approved 2022 roadmap has key initiatives including Ethereum integration and SNS deployment. With the success of the Titanium release, Dfinity’s ability to deliver on its ambitious technical roadmap has become more likely.

NNS Staking - Staking on the NNS has been particularly strong in 2022 compared with 2021. While we won’t know the total ICP staked until neuron indexing is released, I can say with certainty that at least 8M ICP has been staked in known neurons in the last 90 days. It’s possible that newly staked ICP was close to equal the amount of ICP that dissolved off the NNS in Zone 1. If this trend continued, this would set up a strong supply contraction as we enter Zone 2.

Arguments for ICP to Trade less than $40-$60:

New Supply - While Zone 2’s new supply is significantly less than Zone 1’s new supply, it’s still much greater than the amount of ICP that dissolved off the NNS pre-Zone 1. Throughout most of 2021, the NNS shed approximately 2.3M ICP per month, whereas Zone 2 will see average dissolves around 3.3M ICP. This extra million ICP per month should be bearish for the ICP price.

Macro Events - Pre-Zone 1 saw a lot of bullish sentiment in the crypto markets, including Bitcoin and Ethereum making all time highs in November. The macro outlook is much more challenging today, with crypto markets in bearish territory, inflation running high in most of the world and markets in general being on edge due to the Ukraine-Russia conflict.

Summary

The new supply contraction starting in May is a welcome change to anyone who had held ICP for the past few months. It sets up nicely for a possible price floor in the first half of 2022 and price accumulation in the second half of 2022.

However, the story of Zone 2 will be told based on the demand growth of ICP. If the Internet Computer can find a product-market fit that begins to drive significant demand for the ICP token then the steady supply of around 3.5M ICP per month dissolving off the NNS can be easily absorbed by the new demand. Demand could come from any one of DeFi (with Bitcoin and Ethereum integration), NNS staking, SNS tokenization, or continued growth of NFTs on the IC. Any combination of these demand drivers could make ICP deflationary (I previously predicted that circulating ICP would become deflationary in 2024).

It’s unlikely that node rewards or governance rewards will play a significant role (relative to NNS dissolving) in the supply dynamics during Zone 2, so the dissolving ICP is the metric to watch on the supply side. It seems reasonable, given the above arguments, that ICP should trade significantly higher in the second half of 2022 than it has in the first quarter.

Want More?

Please let me know what types of analyses you are interested in. New here? Please subscribe and share.

A light at the end of the tunnel. The tunnel of tokenomic beatings.

Thanks man, love your work