Improving the Financial System

Improving the Financial System

Recent Bank Runs and What We Should Do About Them

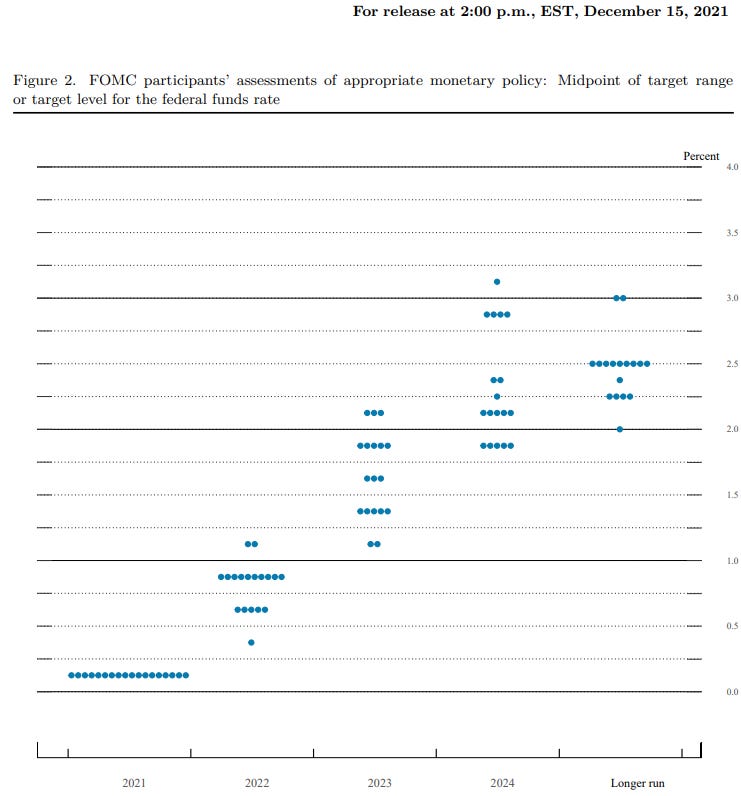

A picture is worth a thousand words and a chart can tell a story. For example, the chart below pretty much tells the entire story about the current financial crisis and the recent bank runs.

The chart above is the federal funds rate projections from the FOMC’s December 15th, 2021 release, the infamous “dot plots”. It shows that the US Fed governors at the end of 2021 expected the Fed fund rates to end 2022 somewhere around 0.75% and for rates to top off in 2024 around 3%. Not a single FOMC participant expected rates to get above even 2.25% in 2022. In actuality, rates finished 2022 at 4.25-4.5% and currently sits as high as 4.75%. In short, even when predicting just 12 months into the future, the every single US Fed leader significantly underestimated the speed in which they would need to raise rates.

Therein lies the root cause of the current financial crisis. Banks made risk decision in 2021 that modeled similar rate hike speeds forecasted by the Fed’s dot plots. When the Fed raised rates faster than expected (the fastest rate of increases in history), all of a sudden the banks’ risk models turned upside-down. It’s easy to forgive the bankers for believing in the Fed’s dot-plot projections; after all, the people making those dot-plot projections are the exact same people who make the decisions whether to raise rates and by how much. When choosing a projection to base your models on, it’s usually wise to trust the projection made by the people who have the most control over whether the projection comes true…

If you think this is an anti-FOMC article, think again. I’m not an armchair economist who thinks he can do better than the professionals. In fact, I think the Federal Reserve gets it right most of the time. It’s not easy to predict the future, especially with something as complicated as the economy, and I do believe the professionals at the Federal Reserve are probably the most competent people in the world at understanding where the economy is and where it might go. The problem, in my opinion, is that even these competent people get it wrong sometimes. And when the Federal Reserve gets it wrong, as they did in 2021, things go really bad.

The Solution

It’s 2023, 94 years after the Great Depression, and we are still suffering from bank runs, albeit less often and less severely. This seems ridiculous as bank runs should be a thing of the past. What do we do though to improve? I’ve seen calls that we need more regulation of the banking industry and I’ve seen arguments that regulation is at the heart of the problem. Both arguments seem logical. And both arguments miss a central point… we are probably near the point of maximum optimization of the current system. The Federal Reserve was created in 1913 and its current structure took shape in the wake of the Great Depression; how likely is it that the current structure can be vastly improved upon, given that we’ve had almost a century to optimize it? It seems, at least to me, that occasional bank runs and the need for a central authority to backstop them, is just an outcome of the current system that will always persist.

Instead we should be recognizing the need for a new system, one that can run parallel to the current centralized system, and one that provides participants in the economy a choice in which system they use for their monetary decisions. Competition is at the root of all that is good about free markets and it’s about time we had competing monetary systems. It’s about time that two systems existed, each holding the other accountable through the risk of capital flight from one to the other.

Obviously, the parallel system I am talking about is blockchain-backed cryptocurrencies that focus on decentralization and premission-less participation. It would be a system built with no central authority, no possibility of bailouts and one in which moral hazard is eliminated. Think Bitcoin + DeFi, but don’t limit yourself to today’s technology and instead think about a system designed from the preferences of the system’s participants in a free market and one in which there is no need or want for centralized planning.

This is not a rally cry to “burn down the current system”, but rather a rally cry to allow competing systems that operate on equal footing. Let the market participants decide which monetary system they prefer, based on their self-interests, and captured in the decisions they make with their capital. Isn’t that type of competition what makes free markets so dynamic and efficient?

A Starting Point

How can our elected officials facilitate the movement to a duopoly monetary system? Quite frankly, ever since the day that Bitcoin went live, the market has been already moving in that direction. Year after year, market participants have moved capital to the decentralized monetary system. The key would be for federal agencies to ensure the blockchain monetary system can compete on equal footing as the current centralized system. Surprisingly, this means smart regulation, not no regulation. Blockchain is currently operating at a massive disadvantage because of regulatory uncertainty. Our elected officials could take these two important first steps:

Write regulations that allow efficient and smooth on-ramps between the two monetary systems. In order for the two systems to compete the touchpoints between them must be as frictionless as possible.

Update the definition of a security to work in a digital world. The current definition was written at a before computers and its about time to update it so the industry can accurately predict what cryptocurrencies will be considered a security.

The way out today’s bank runs may be bailouts to prevent the possible contagion that might stem from bank failures. However, if we want to live in a world in which bank runs and bailouts are not an issue, then we need to significantly rethink our approach to monetary systems, not with marginal changes to regulation of the current system, but with a thriving marketplace of monetary system options. Let the market decide the optimum monetary system, not central authorities.

#WeNeedCompetingMoney

Perhaps it is better to back digitial system with hard currency--in that way you have two independent, one that is very difficult change.

Thanks for the note and agree.